August 29, 2019

A skeptical look at Peloton’s S-1

This was written pre-pandemic but is still interesting considering how the company soared in 2020 only to come crashing back for some of the reasons outlined below.

Here’s the recently released S-1. I was inspired to dig into this a bit because it’s a fun company and I have some good friends that work there. I was also disappointed that the CEO, in ’18, said that the company was “weirdly profitable” while it was losing money on a net income, cash flow, EBITDA, and EBITDA margin basis.

First off, the top-line revenue and subscriber growth is impressive, as is the user engagement. But knowing there will be a lot of swooning over the good stuff, I’m choosing to focus on the pieces that are less clear and, in some cases, not so hot.

To kick it off, here are some high-level concerns:

- There could be a “fad” factor here. Peloton is a relatively new company that’s gotten most of its subscribers in the last 3yrs. There’s a chance its product has a “faddish” component where it’s hyped initially as a novelty by customers, but then that dies down. The bikes could end up sitting in basements and being sold on craigslist for 25% of what customers bought them for in 2022.

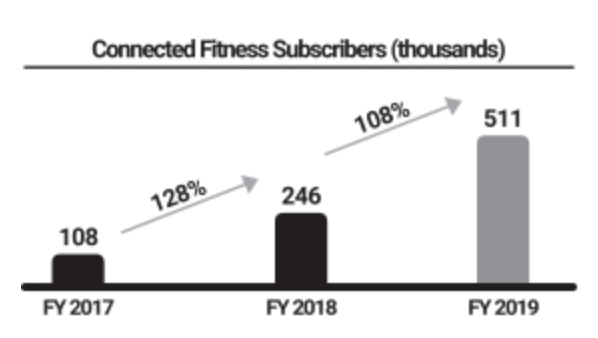

- Long-term subscriber retention is critical, and tough to predict. Today monthly churn for their “Connected Fitness” subscribers is 0.65%, which is super low, and implies the average customer lifetime is 12.8yrs [(1 / 0.65%) * 12)]. Since the company launched their iOS app in ’15, just 4yrs ago, it’s hard to say what subscriber behavior will be like even a few years from now.

- A downturn would likely hit this company harder than most. People have cheaper substitutes. They can ride an actual bike or run outside. They can enroll in a $40/mo gym without paying a $2k upfront cost of a bike. This means that if the economy turns, new bike sales will likely fall and subscriber churn will go up — both bad news.

- Competition will put pressure on pricing and churn. Accelerated competition is guaranteed for a media darling like this — and it’s already happening, here are some examples. This will put some pressure on bike/treadmill pricing, subscription pricing, and could increase subscriber churn because they’ll have other, possibly lower cost or more targeted options.

- The after market will grow, impacting new bike sales. That said, a quick glance on eBay doesn’t show that many bikes for sale, and the ones that are for sale go for a high price point, but this could change quickly as bikes age, the novelty wears off, and (if) the economy turns.

Next, some financial concerns:

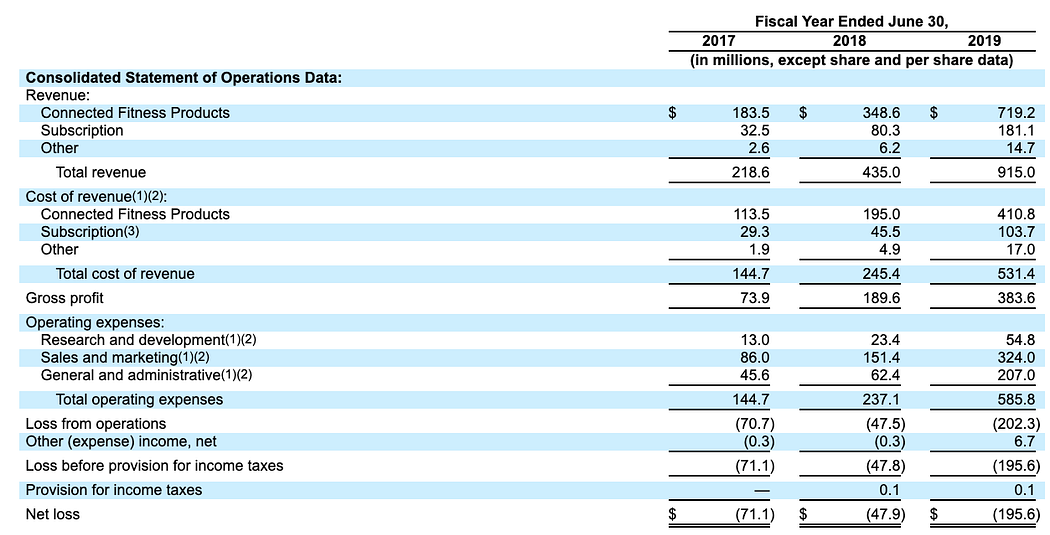

The company is losing $0.21 for every $1.00 in revenue. This is fine if the company’s subscription growth, pricing, and churn numbers continue, but really bad if they don’t because then the company would need to cut headcount rapidly to re-align it’s costs to its revenues. In short, like most startups, the company will do really well if trends continue, and will fall more than most stocks if there’s a hiccup in the markets or their performance.

Also, the losses accelerated significantly in 2019. It only lost $0.11 per $1.00 in revenue in ’18, and $0.21 per $1.00 in ’19.

Peloton income statement —in 2019 it lost $0.21 for every $1.00 in revenue

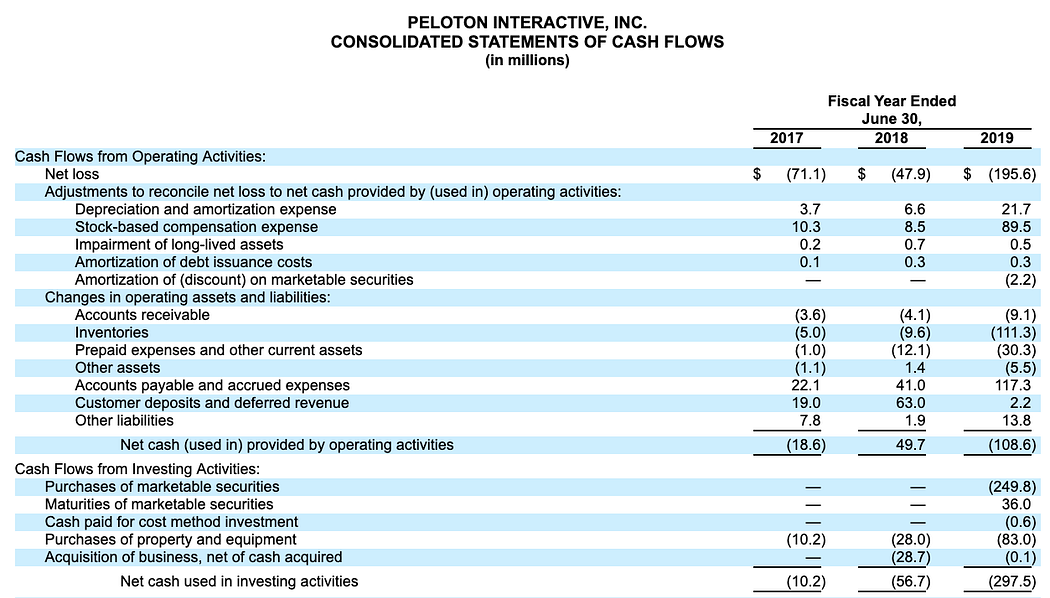

The company also burned about $16m in cash a month in 2019. That’s a lot. However, I do think it’s impressive that they had positive cash flows of $22m, or $1.8m a month, in ’18, while it was growing so rapidly. I would have liked to have seen that “we can growth without burning cash” trend continue into 2019, but I realize that’s rare.

Excerpt from Peloton statement of cashflows —$192m in cash burn (op cash minus PPE) in ‘19

Bike sales are being pushed higher using aggressive offers. Users aren’t paying $2k upfront, they’re essentially buying the bike on a subscription basis. Peloton uses third-party financing partners for this. If customers started to default on these loans at a high rate, then these third-parties would charge peloton more for this financing and they’d likely see lower margins or have to try to pass this additional cost on to the customer. Conversely, if these customer loans perform well, the company could bring financing in-house and earn additional margin on the bike sales.

Some historic digital subscription growth was driven by aggressive offers. This is no longer the case, but it used to be. Given this, company churn could be understated as these previous subscription plans roll off, and subscription growth could be slower going forward because users have to pay for it monthly, immediately.

Until July ’18, the company gave away free subscription months and/or bundled it into the bike sale

Today they charge monthly and don’t advertise a free trial on their site — this is good for the business

Plus side: strong subscription growth has continued, even after the late ’18 shift to a more conservative offering

They should supplement their “workouts per subscriber” metric with an “Avg. workout time per subscriber” so customer engagement is clearer. The number of workouts could increase because shorter workouts are added to the platform and more customers use those. I’d love to see how the “median monthly workout minutes is trending as well.

# of workout per month growing, but there’s no mention of avg. workout time per month

Ok, that’s all I’ve got for now. I must say, there’s a lot to like about the Peloton S-1, most of which I didn’t go into (engagement, contribution margin, revenue growth, possible benefits of scale, network effects) but it’s important to balance that out with a critical analysis of the not-so-hot factors because there’s so much euphoria around VC-backed IPOs in the current market. If you’re going to invest, please try not to pay an exorbitant valuation that’s divorced from the business realities and a risk-adjusted estimate of their future cash flows :)

Happy riding and/or investing!